CONSUMER FINANCIAL PROTECTION BUREAU | SEPTEMBER 2019

Credit Characteristics,

Credit Engagement Tools,

and Financial Well

-Being

Innovation

Insights

1 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

● Éva Nagypál, Ph.D.

● Jeremy Tobacman, Ph.D.

2 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

Executive Summary

This report presents results from a joint research study between the Consumer Financial

Protection Bureau (CFPB) and Credit Karma. Credit Karma describes itself as “a personal finance

technology company” that “offers a suite of products for members to monitor and improve credit

health.”

1,2

The purpose of the study is to examine how consumers’ subjective financial well-being

relates to objective measures of consumers’ financial health, specifically, consumers’ credit report

characteristics. The study also seeks to relate consumers’ subjective financial well-being to

consumers’ engagement with financial information through educational tools. A better

understanding of these relationships helps uncover the factors that work together to determine

consumers’ financial well-being and helps inform the CFPB’s long-term strategy for improving

financial capability.

Financial well-being is measured using the CFPB’s Financial Well-Being (FWB) Scale which

results in a FWB score. The scale was administered through a voluntary survey that resulted in

close to 3,000 de-identified observations on respondents’ FWB score matched with background,

credit report, and website usage data. The main takeaways are as follows:

• A consumer’s credit score is very strongly positively correlated with the FWB score, with a

correlation coefficient of 0.44.

• There is a positive correlation between age and the FWB score, but this correlation all but

disappears when controlling for credit score.

• In addition to credit score and age, the study identifies seven credit report variables and

three engagement variables that correlate strongly with a consumer’s FWB score.

o Credit Report Variables: Credit card limits, holding a credit card, and the number

of accounts recently opened with a balance all correlate positively with a

consumer’s FWB score. Credit card utilization, the number of revolving accounts,

the number of collections in the past two years, and having a student loan all

correlate negatively with a consumer’s FWB score.

o Engagement with Credit Karma Platform Variables: A consumer’s FWB score

correlates positively with the number of times the credit simulator was used and

the number of times credit factors were reviewed. Finally, FWB score correlates

negatively with the number of emails from Credit Karma opened in the last sixty

days.

1

Based on press releases at https://www.creditkarma.com/about/releases. Latest from Jan 24, 2019.

2

Credit Karma is not an agent or affiliate of the CFPB. The CFPB does not endorse Credit Karma, its views, or the

products or services it offers.

3 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

This is the first study of its size to study the relationship between financial well-being and credit

score and other credit report variables, on the one hand, and engagement with financial

information, on the other. The observed correlations might be causal (with changes in the credit

and engagement characteristics in question leading to higher FWB scores) or they might be

explained by reverse causality or omitted variables like the propensity to plan. Either way, the

results are intriguing and warrant further study of these relationships as the CFPB develops its

strategy for improving financial capability using the concept of financial well-being.

4 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

Table of contents

Executive Summary .................................................................................................... 2

Table of contents......................................................................................................... 4

1. Introduction ........................................................................................................... 5

2. Methods and Data ................................................................................................. 7

3. Descriptive Statistics ........................................................................................... 9

4. Correlating Credit Characteristics and Credit Engagement with

Financial Well-Being........................................................................................... 14

4.1 Credit Report Variables ...........................................................................15

4.2 Engagement Variables ............................................................................ 24

5. Summary and Open Questions ......................................................................... 28

Appendix A: ............................................................................................................... 29

Financial Well-Being Scale Questions ............................................................ 29

Appendix B: ............................................................................................................... 30

Matched versus Unmatched Observations ..................................................... 30

Appendix C: ............................................................................................................... 32

Supervised Block-Wise Forward Selection Technical Details ........................ 32

5 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

1. Introduction

An essential part of the mission of the Consumer Financial Protection Bureau (CFPB or the

Bureau) is empowering consumers to take control over their financial lives. Numerous

provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 task the

Bureau with researching, developing, promoting, and implementing financial literacy programs

and activities. In order to measure the success of these efforts, the Bureau undertook rigorous

research to understand and formally define financial well-being in ways that allow it to be

measured and that allow meaningful comparisons between approaches to achieving it.

3

3

CFPB defines financial well-being as a state of being wherein a person can fully meet current and ongoing financial

obligations, can feel secure in their financial future, and is able to make choices that allow enjoyment of life. For

more information on this definition, see “Financial Well-Being: The goal of financial education,” available at

https://www.consumerfinance.gov/data-research/research-reports/financial-well-being/

To

measure the defined concept, the Bureau developed the Financial Well-Being (FWB) Scale, a set

of questions used to measure an individual’s subjective level of financial well-being.

4

.

4

See “Financial Well-Being Scale Development Technical Report,” available at

https://www.consumerfinance.gov/documents/4800/201705_cfpb_financial-well-being-scale-technical-

report.pdf

This scale

was fielded for the first time in 2016 in a nationwide survey of adults in the United States, the

National Financial Well-Being Survey.

5

.

5

See “Financial Well-Being in America,” available at

https://www.consumerfinance.gov/documents/5606/201709_cfpb_financial-well-being-in-America.pdf

The survey collected a variety of self-reported correlates

of financial well-being, such as individual and family characteristics; income; savings; financial

experiences, behaviors, skills, and attitudes. To inform the CFPB’s long-term strategy for

improving financial capability, the CFPB is now interested in better understanding how its

measure of financial well-being relates to objective financial characteristics and to consumers’

engagement with financial information and skill-building opportunities through educational

tools.

Credit Karma is a personal finance technology company that provides consumers with free

access to credit scores, reports, and credit and identity monitoring through web and mobile

interfaces.

6

.

6

See https://www.creditkarma.com/free-credit-score, https://www.creditkarma.com/credit-monitoring, and

http://www.creditkarma.com/id-monitoring

The company also gives members access to free tools, including the Credit Score

Simulator, a variety of loan calculators, and a direct-dispute process to challenge erroneous

credit-report entries.

7

.

7

See https://www.creditkarma.com/tools/credit-score-simulator, https://www.creditkarma.com/calculators/loan

,

and https://www.creditkarma.com/advice/i/credit-karma-direct-dispute.

It uses data modeling to “identify financial products that are a good fit for

6 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

its members”

8

8

Supra note 1.

9

See

and makes money from partners offering these products.

9

https://www.creditkarma.com/about

Because of the nature

of its services, its engagement with a large membership base of more than 100 million

members,

10

.

10

See https://www.bloomberg.com/news/articles/2019-06-21/credit-karma-wants-to-become-your-trusted-credit-

adviser

and its online platform, Credit Karma is well-positioned to provide subjects and an

outlet to study the Financial Well-Being Scale and its correlates among a sample of their

members.

This study took place in the context of the CFPB’s work to encourage consumer-friendly

innovation in markets for consumer financial products and services. As part of the study, Credit

Karma agreed to share insights with the CFPB from a survey on financial well-being and around

peoples’ financial characteristics and engagement with the educational tools on its platform.

11

.

11

See https://www.consumerfinance.gov/about-us/blog/project-catalyst-collaboration-improve-understanding-

financial-well-being/

The study was facilitated by the Office of Research, which provided subject matter expertise in

data and regression analysis. The Office of Financial Education provided advice regarding

financial well-being.

This study has two main goals: (1) to understand how consumers’ subjective assessments of

financial well-being relate to objective financial characteristics measured in credit reports, and

(2) to explore how these assessments of financial well-being relate to engagement on the Credit

Karma platform.

12

.

12

In other work (see supra note 4), the Bureau showed a connection between savings and the habit of savings and

financial well-being. This relationship is not tested for here because savings patterns and balances do not show up

in credit reports.

Financial well-being is measured by surveying Credit Karma members using

the Bureau’s FWB Scale. By linking these survey results to administrative credit report data

(i.e., credit report data in the possession of Credit Karma) for a significant number of

consumers, correlations between objective financial factors and a consumer’s own sense of

financial well-being can be measured. This is also a novel opportunity to study how well-being is

related to a consumer’s propensity to review educational materials, access and monitor credit

reports and scores, and use other tools available on the Credit Karma website. This report covers

the research methodology, implementation details, and analytical results.

7 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

2. Methods and Data

For this project, Credit Karma administered a voluntary survey to some of its members between

September 7, 2017, and October 31, 2017. During the field period, Credit Karma invited

members to participate in the survey when they logged out of their Credit Karma session by

asking, “Before you go, as part of a joint project between Credit Karma and the CFPB, would you

be willing to take a short survey?” Invitations were presented using a quota sampling scheme

13

13

In this quota sampling scheme, Credit Karma members were segmented into mutually exclusive subgroups defined

by age and credit score and a specified number of responses were sought from each subgroup. The number of

responses sought was set to reflect the distribution of Credit Karma members over the age and credit score groups.

For example, 2 percent of Credit Karma members are between the age of 18 and 24 and have a credit score below

700, so the quota for this group was set at 100 (2 percent of 5000). After the quota for a subgroup was reached

during the data collection phase, no more invitations were extended to members of that subgroup.

targeting 5,000 total responses. No member was invited to participate more than once. Credit

Karma users who agreed to take the survey were directed to a Credit Karma/CFPB-branded

page. The survey consisted of the full 10-question version of the CFPB’s Financial Well-Being

Scale. The 10 questions are included as Appendix A. The survey was administered to 4,559

consumers who accepted the invitation, of whom 4,067 provided complete answers. The survey

data also contain the start and end time and date of the survey.

Each respondent’s survey data were then merged by Credit Karma with their background, credit

report, and website usage data. As part of standard business practice, Credit Karma collects

background information on its members, including when they signed up for Credit Karma

services, their state of residence, and their age. In addition, Credit Karma receives credit report

information at every login, conditional on there being at least a one week delay since a prior

credit report refresh. As a result, Credit Karma received up-to-date credit report information,

including credit score, at the time the survey was administered and could match this

information to the survey responses. VantageScore 3.0 credit scores were available at the time of

the survey and each month going back to January 2017 depending upon the length of time that

an individual respondent had been a registered user of Credit Karma. An additional 252 credit

report variables provide information on utilization, performance, and inquiries covering all

major consumer financial product categories (mortgages, credit cards, student loans, auto loans,

and installment loans).

14

14

The credit report information provided is at most seven days old at the time the survey is taken. A consumer’s

credit report is updated upon log-in unless the existing credit report information is less than seven days old. See

https://help.creditkarma.com/hc/en-ca/articles/115004683866-How-often-does-my-credit-report-information-

update-

In addition, several variables provide summary measures across

several categories (e.g., total number of accounts, number of accounts opened in last 6 months).

8 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

Engagement metrics are also collected in the normal course of Credit Karma’s operations.

Relevant variables include the number of educational articles viewed by a member, the number

of times they viewed their TransUnion or Equifax credit report information, the number of

times they disputed credit report information, and whether they used the Credit Score Simulator

tool over the previous 30, 60, and 90 days. Overall, Credit Karma provided 75 variables

regarding member engagement and use patterns. These variables were merged by Credit Karma

with the survey and credit report data listed above.

The data thus collected and matched by Credit Karma were provided to the CFPB after removing

any information that could directly identify, or reasonably be linked to, an individual consumer.

Of the 4,067 completed survey responses, Credit Karma provided matched credit report and

engagement data for 2,966 respondents. Appendix B compares the matched and unmatched

observations in terms of their age and Financial Well-Being Score and finds that they are very

similar. All of the analysis that follows is based on the 2,966 matched observations.

9 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

3. Descriptive Statistics

The FWB Score is an individual’s score on the CFPB Financial Well-Being Scale and is a

standardized number between 0 and 100 that quantifies that person’s underlying level of

financial well-being. The questions that make up the scale were presented in the Credit Karma

survey, which allowed Credit Karma then to calculate a FWB score for each respondent.

Figure 1: Distribution of Financial Well-Being Score in the Credit Karma survey and in the

CFPB’s National Financial Well-Being survey

Figure 1 shows the distribution of FWB score among the nationally representative sample of

U.S. adults included in the CFPB’s National Financial Well-Being Survey and among the Credit

Karma respondents.

15

As can be seen, the distributions are quite similar, with the notable

difference that Credit Karma respondents are significantly less likely to have low FWB scores

15

The micro data used here from the CFPB’s nationally representative survey about financial well-being have also

been publicly released. For more information including data access, see “National Financial Well-Being Survey

Public Use File User’s Guide,” available at https://files.consumerfinance.gov/f/documents/cfpb_nfwbs-puf-user-

guide.pdf.

10 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

(scores of 40 or below) and are somewhat less likely to have very high FWB scores (scores above

70). Instead, the scores of Credit Karma members are more concentrated towards the middle.

Figure 2: Financial Well-Being Score as a function of age: functional approximation with

confidence intervals and average and interquartile range (IQR) by age group

Figure 2 shows the relationship between FWB score and age using two methods: first, displaying

the relationship between the two using a flexible technique that allows one to uncover a smooth

relationship between two variables (known as “local polynomial smoothing”) and second

showing the average FWB score and the range between the 25

th

and 75

th

percentile (the

interquartile range) by age group. Both methods clearly show that the FWB score is constant on

average at a score of around 56 until age 40, after which it starts to rise, reaching over 60 by age

70. This is again in line with the findings of the National Financial Well-Being Survey, which

also found increases with age, especially after 40, albeit from a somewhat lower base of 51 for

those aged 34 and younger.

16

The interquartile ranges are between 13 and 15 points which

demonstrates that there is substantial variation in FWB score within each age group.

16

See “Financial Well-Being in America,” supra note 4, Figure 7, p. 31.

11 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

Figure 3: Financial Well-Being Score as a function of VantageScore 3.0 credit score: functional

approximation with confidence intervals and average and interquartile range by credit score

decile

Next, Figure 3 shows the relationship between FWB score and credit score

17

using the same two

methods as above: first, displaying the relationship between the two using a local polynomial

smoothing and second showing the average FWB score and its interquartile range for each credit

score decile. A credit score measures a consumer’s creditworthiness based on data from the

consumer’s credit report that generally reflects credit use and repayment history. Since credit

scores are based on algorithms derived from third-party data from a consumer’s financial life,

they are considered objective measures of a consumer’s credit risk.

18

As is clear from the figure, the FWB score (which is designed to measure the inherently

subjective concept of financial well-being) is strongly positively related to a consumer’s credit

score (which is designed to be an objective measure of creditworthiness). In fact, the correlation

17

The credit score contained in the data is the VantageScore 3.0 score.

18

These objective credit report measures complement the objective financial situation measures (income retirement

status, etc.) that were studied in “Pathways to financial well-being: Research brief,” available at

https://www.consumerfinance.gov/data-research/research-reports/pathways-financial-well-being/.

12 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

between the two variables is 0.44 and credit score by itself explains 19.7 percent of the variation

in FWB scores across the respondents in the data. The average FWB score among consumers in

the bottom 10 percent of the credit score distribution is 46.7 while the average among those in

the top 10 percent is 65.0. While it is not surprising that the correlation between the FWB score

and the credit score is positive and strong, this report is the first one to document the

relationship between individuals’ assessment of their financial well-being and their

creditworthiness.

It is worth noting that while the documented relationship is strong, over 80 percent of the

variation in FWB score cannot be explained by one’s credit score, possibly indicating that the

FWB score is a more complex measure than credit score and is influenced by factors beyond

creditworthiness and access to credit. The interquartile range within each credit score decile is

12 to 14 points, implying that there is substantial variation in FWB score within these deciles.

The next section explores further other factors in the data that are correlated with the FWB

score.

Figure 4: Financial Well-Being Score as a function of age: the effect of controlling for credit

score

Before turning to those analyses, Figure 4 documents that most of the observed variation in

FWB score with age is related to the fact that, on average, a consumer’s credit scores increase

13 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

with age. The figure shows the relationship between the average FWB score and age with and

without controlling for credit score. The strong positive relationship that exists between the

FWB score and age after age 40 (shown by the steep line in Figure 4) all but disappears when

controlling for credit score.

14 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

4. Correlating Credit

Characteristics and Credit

Engagement with Financial

Well-Being

As outlined in the Methods and Data section, for each Credit Karma member in the study, 252

credit report variables and 75 engagement variables are observed. To identify variables that are

important correlates of the FWB score in addition to credit score and age,

19

19

In the regression model, the coefficient on age is allowed to change at age 40.

a variable selection

method known as supervised block-wise forward selection is performed. The details of this

method are described in Appendix C.

This method selected seven credit report variables and three engagement variables that are

statistically significant correlates of a consumer’s FWB score in a multivariate regression model.

The graphs below present 1) the relationship between each of these variables and the FWB score

without any controls, and 2) the marginal effect of the variable on the FWB score controlling in

each case for credit score, age, and the other nine selected variables. The marginal effect results

from running the multivariate regression model with credit score, age, and all the selected

variables included, and then plotting the effect of each variable separately holding the other

explanatory variables constant at their means.

It is imperative to keep in mind that the relationships found do not imply that selected variables

cause the FWB score to increase. Such a conclusion cannot be drawn from a cross-sectional

research design such as this one. To demonstrate what the results do mean, consider the

example of credit simulator use. The credit simulator use results say that consumers who use

the credit simulator tend to a have higher FWB score in the cross-section, even after controlling

for many other observable characteristics of the consumer. The relationship could be a result of

credit simulator use causing the FWB score to increase (causality), consumers with a higher

FWB score choosing to use the credit simulator more often (reverse causality), or a third,

omitted variable (such as, for example, a propensity to plan), affecting both outcomes (omitted

variable bias).

It is also worth noting that several of the selected credit report variables are strongly correlated

with credit score. This is either because they are directly included in credit scoring models (e.g.,

15 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

utilization) or are determined in part by credit score (e.g., credit limit). Given that both credit

score and the other selected variables are included in the regression model, the additional effect

of the selected variables above and beyond the effect coming through the credit score can be

parsed out. This additional effect is what the marginal effects reported below capture.

4.1 Credit Report Variables

In this section, important credit report correlates of the FWB score are identified. Table 1 shows

the credit report variables selected by method outlined above, the sign of their conditional

correlation with the FWB score, and the marginal effect as each selected variable moves across

interquartile range of its distribution (or as it moves from 0 to 1 in the case of variables that take

on only these two values).

Table 1: Summary of effect of selected credit report variables on FWB score

Selected variable

Conditional

correlation

Interquartile

effect*

Credit score + 4.99

Credit card limit + 2.23

Utilization of bank card - 1.97

Number of revolving accounts - 1.83

Number of collections in past two years - 1.45

Has a bank card + 2.48†

Number of accounts opened w/ balance + 0.80

Has student loan - 0.98†

*Effects reported are interquartile effects except for 0/1 variables marked with † for which the effect of

moving from 0 to 1 is reported.

16 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

Figure 5: Financial Well-Being Score as a function of total credit card limit: raw data by deciles

and marginal effect based on regression model

F

igure 5 shows the relationship between a consumer’s total credit card limit and FWB score. The

small circles represent average FWB score in the data within each credit card limit decile. The

solid line represents the regression model-implied relationship between the FWB score and

credit card limit once credit score and the other control variables are taken into account. As can

be seen, there is a strong positive relationship between FWB score and credit card limit without

any further controls (i.e., in the raw data). Of course, much of this is due to the fact that both

credit card limit and the FWB score increase with a consumer’s credit score. The solid line

implies, however, that there is a positive relationship between credit card limit and the FWB

score even after controlling for credit score and the other control variables. This implies that

given two consumers with identical credit scores and identical values on the other control

variables, the one with the higher credit card limit is expected to have a higher FWB score. The

marginal effect is reported as the predicted change in FWB score as the credit card limit moves

across the interquartile range of its distribution. The reported marginal effect of 2.23 in Figure 5

then means that as one moves from the 25th percentile of the credit card limit distribution

($3,700, marked as “p25” in the figures) to the 75th percentile ($40,800, marked as “p75” in the

figures) holding all other model variables (credit score, age, and other selected variables)

17 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

constant, the FWB score is expected to increase by 2.23 points.

20

20

In other words, the interquartile range is defined as moving from the 25

th

to the 75

th

percentile. These percentiles

in turn are defined based on the observation that out of every 100 representative consumers, 25 have credit limits

below $3,700, the 25

th

percentile, and 25 have credit limits above $40,800, the 75

th

percentile.

As a comparison, the

regression model implies that moving across the interquartile range of the credit score

distribution (from 652 to 780) increases the FWB score by 4.99 points. The 0.29 reported in

parentheses is the corresponding standard error.

The fact that this conditional correlation is positive could be due to the fact that total credit limit

increases with income or education, for example, which themselves have a positive relationship

with the FWB score. It could also be due to the direct impact of more access to credit on the

FWB score. Since a direct measure of income or education is not available, it is not possible to

assign appropriate weights to these alternative explanations.

Figure 6: Financial Well-Being Score as a function of the utilization of general purpose credit

cards: raw data by deciles and marginal effect based on regression model

18 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

Figure 6 shows the second most predictive of the selected variables: utilization of general

purpose credit cards.

21

The graph is structured similarly to above: the small circles represent the

raw relationship between utilization and the FWB score, while the solid line shows the marginal

effect of utilization keeping credit score, age, and the other selected variables constant. There is

a negative relationship between utilization and the FWB score both in the raw data and in the

regression analysis. Again, the marginal effect from the regression shows a more muted

relationship than the raw data, which is due to the fact that utilization is significantly correlated

with credit score. This correlation implies that consumers with a low credit score and high

utilization have a lower FWB score. The negative marginal effect means that utilization is

negatively related to the FWB score above and beyond its effect through the credit score.

Quantitatively, the predicted change as utilization moves across the interquartile range of the

distribution from 3 percent (25

th

percentile) to 55 percent (75

th

percentile) is a decrease of 1.97

points on the FWB score, with a standard error of 0.36.

21

General purpose credit cards (called “revolving bank cards” in credit reporting terminology) comprise the majority

of credit cards and are general-use cards branded by a financial institution that allow the consumer to revolve a

balance. (The card is considered revolving if it allows for balances to be revolved, regardless of whether consumers

take advantage of this feature. We do not directly observe in our data whether balances are revolved or not by

consumers.) Other large categories of credit cards are retail credit cards branded by and useable at department

stores and other retailers and charge cards branded by financial institutions that do not allow the consumer to

revolve a balance.

19 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

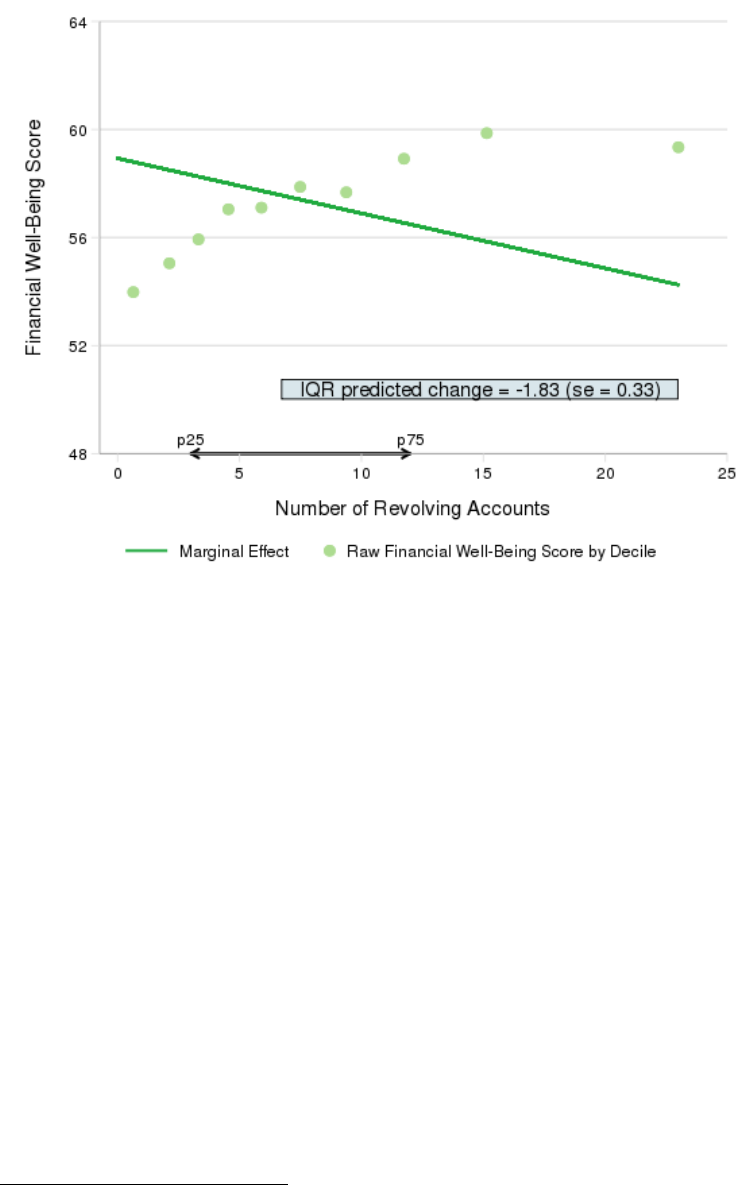

Figure 7: Financial Well-Being Score as a function of the number of revolving accounts: raw

data by deciles and marginal effect based on regression model

Figure 7 shows the third most predictive of the selected variables: number of revolving

accounts.

22

Here the raw relationship between FWB score and the number of revolving accounts

is positive: people with more revolving accounts have higher FWB scores. This can once again be

explained by the correlation with credit score: consumers with higher credit scores tend to have

more revolving accounts. Once credit score is controlled for, however, considering two

consumers with the same credit score (and the same values for the other model variables), the

one with more revolving accounts is likely have a lower FWB score. In terms of size, the

predicted change here is slightly lower: as the number of revolving accounts moves across the

interquartile range of the distribution from three accounts (25

th

percentile) to 12 accounts (75

th

percentile), the FWB score is expected to decrease by 1.83, with a standard error of 0.33.

22

Here revolving accounts include both revolving bank card and revolving retail card accounts.

20 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

Figure 8: Financial Well-Being Score as a function of the number of collections first reported in

the last 24 months: raw data by deciles and marginal effect based on regression model

Figure 8 shows the next most predictive of the selected variables: number of collections first

reported in the last 24 months. While close to 83 percent of the consumers do not have any

collections reported in the preceding two years, 9 percent do have one and 8.5 percent have

more than one. Having more collections is strongly negatively associated with a consumer’s

FWB score even after controlling for credit score and the other variables in the model. As the

number of collections moves across the interquartile range of the distribution from one to three

collections (among those with a collection), the FWB score is expected to decrease by 1.45, with

a standard error of 0.39.

Figure 9 shows a variable that captures whether a consumer has a general purpose credit card.

This variable can take on only the value 0 (corresponding to not having a general purpose credit

card) or 1 (corresponding to having a general purpose credit card). This means that there are

only two small circles on the graph, corresponding to the average FWB score for those who do

not and those who do have a general purpose credit card (51.3 and 58.2, respectively). Again,

some of the difference is muted when controlling for credit score and the other model variables.

The two diamonds on the graph correspond to these marginal effects. Going from not having a

general purpose credit card to having a general purpose credit card increases the FWB score by

2.48, with a standard error of 0.72. Notice that this is not directly comparable to the earlier

21 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

marginal effects for continuous variables where a change equivalent to the interquartile range

was considered.

Figure 9: Financial Well-Being Score as a function of whether consumer has general purpose

credit card: raw data by category and marginal effect based on regression model

22 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

Figure 10: Financial Well-Being Score as a function of number of accounts opened in last 12

months with a balance: raw data by decile and marginal effect based on regression model

Figure 10 shows the relationship between the FWB score and the number of accounts that the

consumer opened in the last 12 months that carry a balance.

23

Here the raw relationship

between the FWB score and the number of such accounts is not very strong, but the regression

analysis uncovers a somewhat positive conditional correlation: as the number of accounts moves

across the interquartile range of the distribution, the FWB score is expected to increase by 0.80,

with a standard error of 0.25. As before, this need not imply a causal relationship, and could be

due to selection on variables (such as income) that are not observed in our study.

Finally, Figure 11 depicts the relationship between having a student loan and the FWB score.

This again is a variable that can take on only the value 0 (corresponding to not having any

student loans) or 1 (corresponding to having some student loans). The corresponding two small

circles on the graph show that the average FWB score for those who do not have a student loan

is 58.3 and 54.6 for those who do have student loans. Of course, consumers with student loans

are different from consumers without such loans (notably, they are younger on average). The

regression model uncovers that the marginal effect of having a student loan versus not having

23

In some figures there are fewer than ten points representing the deciles. This happens when multiple deciles take

on the same value due to the concentration of observations on certain values.

23 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

one (shown by the diamonds in Figure 11) is a decrease in the FWB score of 0.98 (with a

standard error of 0.46), where this effect controls for the other model variables, including age.

Again, this is not directly comparable to the earlier marginal effects for continuous variables.

Figure 11: Financial Well-Being Score as a function of whether consumer has student loans:

raw data by category and marginal effect based on regression model.

24 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

4.2 Engagement Variables

In this section, important engagement correlates of the FWB score are identified. Table 2 shows

the engagement variables selected by method outlined above, the sign of their conditional

correlation with the FWB score, and the marginal effect as each selected variable moves across

interquartile range of its distribution.

Table 2: Summary of effect of selected variables on FWB score

Selected variable

Conditional

correlation

Interquartile

effect

Number of times credit simulator used + 0.42

Number of times credit factors reviewed + 0.50

Number of emails opened in last 60 days - 0.53

The block-wise forward selection procedure highlighted three engagement variables as

significant correlates of the FWB score.

24

24

See Appendix C for details.

These correlations are reported in the next three

figures using the same methodology as above, i.e., showing the raw correlations and the

marginal effect controlling for all other selected variables.

Credit Karma offers a Credit Score Simulator tool to its members. This is an educational tool

that starts with the information in the consumer’s credit report and explores how changing that

information could affect the consumer’s score. Figure 12 shows the raw relationship between

the number of times a consumer used the credit simulator tool and the FWB score and the

marginal effect of using the simulator.

25

There is not a strong relationship between the two

measures in the raw data, but the regression analysis uncovers a somewhat positive and

statistically significant conditional correlation: as simulator use moves across the interquartile

range of the distribution,

26

the FWB score is expected to increase by 0.42 (with a standard error

of 0.17). While this change is smaller than that induced by the credit report variables, according

to the regression model, it is equivalent to the change associated with a credit limit increase of

$7,000, a sizable increase.

25

Note that the number of times the simulator was used is top-coded at the top three percentile. There are some very

large counts for this variable in the data, most likely accounted for by how website usage and reload is recorded as

opposed to actual use.

26

Note that due to the large share of members who do not engage with Credit Karma’s tools (47.1 percent for the

Credit Score Simulator, 68.6 percent for the credit factors, and 69.8 percent for the email within 60 days), for the

engagement variables the interquartile range is defined among members who engage with the respective tool at

least once.

25 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

Figure 12: Financial Well-Being Score as a function of the number of times the credit simulator

is used: raw data by decile and marginal effect based on regression model

Credit Karma offers another educational tool to its members, one that allows members to better

understand the factors that affect credit scores in general and that member’s credit score in

particular. Figure 13 shows the raw relationship between the number of times a consumer

reviewed the credit factors and the FWB score and the marginal effect of reviewing the credit

factors. Again, there is not a strong relationship between the two measures in the raw data, but

the regression analysis uncovers a statistically significant positive conditional correlation: as

credit factor use moves across the interquartile range of the distribution, the FWB score is

predicted to increase by 0.50 (with a standard error of 0.14). According to the regression model,

it is equivalent to a change associated with a credit limit increase of $8,300, a sizable increase.

Again, this is a relationship that deserves further study to determine any possible causality.

26 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

Figure 13: Financial Well-Being Score as a function of the number of times credit factors are

reviewed: raw data by decile and marginal effect based on regression model

Credit Karma routinely emails their members with information, suggestions, and credit

monitoring alerts. Members can opt in to some categories of email and opt out of most

categories. As Figure 14 demonstrates, the number of emails opened within the past 60 days is

negatively correlated with the FWB score both in the raw data and in the regression model.

Choosing to open many emails could be an indication of concern about one’s financial situation,

an increase in changes on credit reports, or it could imply information overload. Or the

relationship could be due to omitted variable bias. Again, the data do not allow researchers to

determine the mechanism. Moving across the interquartile range of the opened email count

distribution, the FWB score decreases in expectation by 0.53 (with a standard error of 0.25),

which is equivalent to the change associated with a credit limit decrease of $8,800.

27 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

Figure 14: Financial Well-Being Score as a function of the number of emails opened in last 60

days: raw data by quintile and marginal effect based on regression model

28 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

5. Summary and Open

Questions

This collaboration has brought together Credit Karma, a personal finance technology company

providing free credit scores and reports and credit-related educational tools, and the CFPB to

study new survey data to understand the relationship between Financial Well-Being as

measured by the FWB score, credit report variables, and variables summarizing engagement

with Credit Karma’s platforms.

Ten variables were identified– in addition to age and credit score – that correlate strongly with a

consumer’s Financial Well-Being score. Among variables found on credit reports, credit card

limits, holding a credit card, and the number of accounts recently opened with a balance all

correlate positively with a consumer’s FWB score. Credit card utilization, the number of

revolving accounts, the number of collections in the past two years, and having a student loan all

correlate negatively with a consumer’s FWB score.

Among variables characterizing engagement with Credit Karma’s platform, a consumer’s

Financial Well-Being score correlates positively with the number of times the credit simulator

was used and the number of times credit factors were reviewed. FWB score correlates negatively

with the number of emails opened in the last sixty days.

This report’s findings are intriguing and novel. No prior work has studied the relationship

between financial well-being and engagement with financial information using administrative

engagement data. Only one other exploratory project linked FWB score with credit report data

to date, but with a much smaller sample. The observed correlations might be causal, or they

might be explained by reverse causality or omitted variables like the propensity to plan. Either

way, the results are intriguing and warrant further study of these relationships as the CFPB

develops its strategy for improving financial capability using the concept of financial well-being.

29 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

APPENDIX A:

Financial Well-Being Scale

Questions

Table 3: Ten-question version of Financial Well-Being Scale

Questions

Statement

Response Options

How well does

this statement

describe you or

your situation?

1. I could handle a major unexpected

expense.

2. I am securing my financial future.

3. Because of my money situation, I feel

like I will never have the things I want in

life.*

4. I can enjoy life because of the way I’m

managing my money.

5. I am just getting by financially.*

6. I am concerned that the money I have or

will save won’t last.*

• Describes me

completely

• Describes me very

well

• Describes me

somewhat

• Describes me very

little

• Does not describe me

at all

How often does

this statement

apply to you?

7. Giving a gift for a wedding, birthday or

other occasion would put a strain on my

finances for the month.*

8. I have money left over at the end of the

month.

9. I am behind with my finances.*

10. My finances control my life.*

• Always

• Often

• Sometimes

• Rarely

• Never

* More affirmative responses indicate lower levels of financial well-being

30 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

APPENDIX B:

Matched versus Unmatched

Observations

As reported in the main text, 4,067 Credit Karma customers responded to the financial well-

being survey. 2,966 of these customers had matched data on credit reports and engagement. In

this appendix, it is examined whether the distribution of observable variables (FWB score and

age) are different across the matched and unmatched observations. The kernel density estimates

in Figure 15 and 16 indicate that the distributions are very similar. This suggests that any bias

from considering only the matched observations in the study is likely small.

Figure 15: Kernel density estimate of distribution of Financial Well-Being Score among

unmatched and matched observations

31 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

Figure 16: Kernel density estimate of distribution of age among unmatched and matched

observations

32 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

APPENDIX C:

Supervised Block-Wise

Forward Selection Technical

Details

Block-wise forward selection with supervision is a transparent method for choosing explanatory

variables for exploratory statistical analysis. The objective is not to discern causal relationships,

but rather to focus attention on variables that correlate strongly with the main variable of

interest (Financial Well-Being score, in this case).

The variables are first preprocessed as follows. Four variables without any within-sample

variation and 13 variables with fewer than 1% of observations having non-zero values are

dropped. Two variables are dropped due to being too aggregated and one variable due to being

very highly correlated with a similar variable. Next, each variable that has a “Not applicable”

value is coded as follows: for the observations with a “Not applicable” value originally, a value of

0 is assigned. Then an indicator value is defined which takes on the value of 1 for observations

with a “Not applicable” value originally, and 0 otherwise. This allows one to keep all

observations in the dataset, but allow for “Not applicable” values to enter flexibly.

First, one credit score among several that were provided is chosen, the VantageScore 3.0 score.

Next, credit report variables are considered. From this set of variables, first all performance

related variables (various measures of being past due or delinquent) are excluded from

consideration. The credit score is a summary variable reflecting expected loan performance, so

this exclusion assures that the data are not overfitted (overfitting occurs when a model

unintentionally extracts some of the noise as if that variation represented underlying model

structure). Then the rest of the credit report variables are partitioned into the following mutually

exclusive and collectively exhaustive blocks: mortgage loan and home equity line of credit

variables, student loan variables, auto loan variables, installment loan variables, credit card

utilization variables, other credit card variables, summary utilization variables, and other

summary variables. Two final blocks consist of collection and inquiry related variables, which

are excluded from the loan type blocks.

33 CREDIT CHARACTERISTICS, CREDIT ENGAGEMENT TOOLS, AND FINANCIAL WELL-BEING

Within each block, the algorithm selects variables using the following process. The algorithm

sets the set of provisionally selected variables to the null set. This set of provisionally selected

variables is updated by adding explanatory variables as follows, at most one per round. In each

round, the algorithm passes through all unselected variables, one by one, and regresses the

Financial Well-Being score on age, allowing for a different slope over age 40, the credit score,

the existing set of provisionally selected variables, and the candidate explanatory variable. In

each regression only the variation between the 25th and 75th percentiles of the candidate

variables’ distribution is used, conditional on the candidate variables being positive. This is done

because it is not desirable to have the observed relationship to be driven only by outliers. A

candidate explanatory variable is added to the set of provisionally selected variables if two

conditions are met: 1) it is statistically significant at the 90 percent level of confidence and 2) the

R^2 from the regression with this variable is higher any other R^2 observed during the current

round. If a round does not produce any candidate explanatory variable that satisfies these

conditions, then the algorithm stops and the set of provisionally selected variables is finalized.

After each round that produces an additional selected variable, any variable from the set of

provisionally selected variables that fails to continue to be statistically significant at the 90

percent level of confidence is dropped. After implementing this algorithm within each block, the

same algorithm is run, pooling all the block-level selectees using appropriate supervision.

After selecting credit report variables, the engagement variables are selected using a very similar

methodology. These variables are partitioned into four blocks, covering recent logon

frequencies; responsiveness to offers measured by views and clicks; the duration since joining

Credit Karma; and all the remaining engagement measures. The engagement variables are

treated differently in two ways. First, while selecting engagement variables both within and

between blocks, the selected credit report variables are controlled for. Second, when selecting

the engagement variables, attention is not restricted to observations between the 25th and the

75th percentile since there is less inherent variation in these variables, as many consumers do

not engage with the available tools. To limit the influence of outliers, here topcoding is used.

Note that the process never selects between credit report and engagement variables

simultaneously. Exploration of both these domains is important, novel, and therefore merits

positive attention.