Annual ADFSL Conference on Digital Forensics, Security and Law

2014

Proceedings

May 29th, 9:00 AM

Computer Forensics for Accountants Computer Forensics for Accountants

Grover S. Kearns

College of Business, University of South Florida St. Petersburg

(c)ADFSL

Follow this and additional works at: https://commons.erau.edu/adfsl

Part of the Aviation Safety and Security Commons, Computer Law Commons, Defense and Security

Studies Commons, Forensic Science and Technology Commons, Information Security Commons,

National Security Law Commons, OS and Networks Commons, Other Computer Sciences Commons, and

the Social Control, Law, Crime, and Deviance Commons

Scholarly Commons Citation Scholarly Commons Citation

Kearns, Grover S., "Computer Forensics for Accountants" (2014).

Annual ADFSL Conference on Digital

Forensics, Security and Law

. 12.

https://commons.erau.edu/adfsl/2014/thursday/12

This Peer Reviewed Paper is brought to you for free and

open access by the Conferences at Scholarly Commons.

It has been accepted for inclusion in Annual ADFSL

Conference on Digital Forensics, Security and Law by an

authorized administrator of Scholarly Commons. For

more information, please contact [email protected].

ADFSL Conference on Digital Forensics, Security and Law, 2014

143

COMPUTER FORENSIC PROJECTS FOR ACCOUNTANTS

Grover S. Kearns, Ph.D., CPA, CFE, CITP

College of Business

University of South Florida St. Petersburg

140 7th Avenue South

St. Petersburg, FL 33701

Phone: 727-873-4085

Cell: 727-688-8733

ABSTRACT

Digital attacks on organizations are becoming more common and more sophisticated. Firms are

interested in providing data security and having an effective means to respond to attacks. Accountants

possess important investigative and analytical skills that serve to uncover fraud in forensic

investigations. Some accounting students take courses in forensic accounting but few colleges offer a

course in computer forensics for accountants. Educators wishing to develop such a course may find

developing the curriculum daunting. A major element of such a course is the use of forensic software.

This paper argues the importance of computer forensics to accounting students and offers a set of

exercises to provide an introduction to obtaining and analyzing data with forensics software that are

available free online. In most cases, figures of important steps are provided. Educators will benefit

when developing the course learning goals and curriculum.

Keywords: Computer forensics; forensic accounting; accounting education

1. INTRODUCTION

Increased reliance on both technological and accounting skills has been recognized in research

(Albrecht and Sack, 2000; Tan et al., 2004). The increase of digital fraud has led many accountants to

acquire advance information technology (IT) skills and certifications in order to qualify as IT auditors

and forensic accountants (Davis et al., 2007). As routine accounting tasks are becoming highly

automated an accountant’s value is more likely to be determined by higher order skills such as those

needed in forensic analysis (Hunton, 2002).

A data breach can result in extensive losses in both profits and reputation. The Target data breach that

affected as many as 110 million customers received substantial adverse publicity and the total dollar

loss is expected to be high (LA Times).

Companies may be legally obligated to provide confidentiality. Failure to protect personally

identifiable information (PPI) may subject the organization to fines and other penalties. The Gramm-

Leach-Bliley Act and Health Insurance Portability Act stipulate that financial and health organizations

are accountable for the safe guarding of PPI (Pearson, 2008) and firms that operate abroad may be

subject to the European Union Data Protection Directive which places stringent rules on the protection

of private information.

Professional and regulatory bodies recognize the value of IT to accountants. The American Institute of

Certified Public Accountants recognizes the importance of technology to the organization and to

accountants. In its 2013 List of Top 10 Technology Initiatives the AICPA listed “Securing the IT

Environment”, “Ensuring Privacy” and “Preventing and Responding to Computer Fraud” as top

priorities (AICPA, 2013). The Public Company Accounting Oversight Board (PCAOB) has

recommended that auditors receive IT training (O ’Donnell and Moore, 2005). An analysis of 595 job

ADFSL Conference on Digital Forensics, Security and Law, 2014

144

listings for IT auditors found that a large percentage specifically mentioned technical skills/abilities

including networking, security, database, experience with IT controls, and computer-assisted audit

tools and techniques (Merhout and Buchman, 2007). The Sarbanes-Oxley Act of 2002 and SAS No.

99 (SAS 99), “Consideration of Fraud in a Financial Statement Audit,” extended expectations for

auditors stating that,

“Electronic evidence often requires extraction of the desired data by an auditor with

IT knowledge and skills or the use of an IT specialist … it may be necessary for the

auditor to employ computer-assisted audit techniques … to identify the journal

entries and other adjustments to be tested.”

The increased sophistication and complexities of information systems have created vulnerabilities that

can be exploited to damage organizations by compromising confidential personal information,

allowing unauthorized access to sensitive projects and intellectual property, and by concealing

financial statement frauds and misappropriation of assets. In order to assess the nature and extent of

these threats, to acquire and analyze evidence and to maintain a proper chain of custody, forensic

accountants must possess a basic understanding of computer forensic techniques. This paper presents a

set of exercises and projects that will be useful to educators creating an introductory course in

computer forensics for accountants. This provides and important element in curriculum development

and allows students to learn these skills in a hands-on environment. The exercises and projects use

widely recognized software that is freely available.

2. COMPUTER FORENSICS FOR ACCOUNTANTS

Nelson et al. (2010) define computer forensics as “The process of applying scientific methods to

collect and analyze data and information that can be used as evidence.” Thus, computer forensics

addresses the methods and procedures necessary to investigate possible criminal and non-criminal

conduct involving digital data. From an organizational perspective, investigations should initially

proceed with the assumption that the case may be of a criminal nature so that all steps meet the

statutory rules for admission of evidence. An understanding of computer forensics allows the

accountant to make knowledgeable decisions regarding what steps to take and how to proceed during

an investigation and not taint the evidence.

Computer forensics is considered by some to be dominated by IT and law-enforcement. Although both

play important roles, there are reasons that forensic analysis requires the attention of accountants.

Accountants, in particularly auditors, are highly familiar with corporate information systems (IS),

policies and internal controls, and possess advanced analytical skills. Neither IT nor law-enforcement

have a broad understanding of the overall systems and databases, access rights, organizational roles

and responsibilities which are critical to an effective forensic investigation. Furthermore, they may

have priorities that may not parallel and could even conflict with organizational needs. For these

reasons, the combination of accounting and computer forensics provides an unmatched capability to

investigate, analyze and report on suspicious patterns and anomalies and to follow the trail of

unauthorized activities (Kearns, 2010).

Most firms have one or more internal auditors with forensic skills who are responsible for fraud

detection and investigation (Pearson et al., 2008). Evidence in most organizational fraud cases is in

digital form. With the need for increased vigilance it is imperative that these professionals be able to

obtain, manage, and analyze digital forensic data in an effective manner. These accountants need, at

minimum, training in the basics of computer forensics.

3. COMPUTER FORENSIC TRAINING

IT is now considered a basic skill for accountants (Hurt, 2007) and most undergraduate accounting

students acquire an intermediate level IT competency. AACSB accredited schools usually include

ADFSL Conference on Digital Forensics, Security and Law, 2014

145

three courses in computer related knowledge and skills. First is an introductory computer class that

covers productivity software including word processing, spreadsheets, database, email and slide

presentation software. Second is a management information systems (MIS) class that covers the

foundations of information resources, system management and security techniques, database concepts

and IS management principles. Third is a course in accounting information systems (AIS) that focuses

on internal controls for IS, transaction systems, systems design and documentation, system security,

computer fraud, and IT governance. The AIS class may also cover advanced spreadsheet and database

knowledge and generalized audit software such as Audit Control Language (Coglitore and Matson,

2007).

Some accounting programs now offer courses in forensic accounting and a few colleges have full

programs in forensic accounting. Graduate programs may offer an emphasis or track in forensic

accounting in the MBA or Masters of Accountancy programs. The composition of the courses varies

depending upon the number of courses offered. Schools that offer a full program or major will have a

broader offering than those that only offer an emphasis or track in forensic accounting. Acquiring

these skills can increase market appeal particularly for accounting students who wish to work as

internal auditors or as IT or fraud auditors or as agents for the IRS or FBI. As a result of the increasing

need for digital security and the importance of uncovering corporate fraud many universities are also

creating courses in computer forensics (Busing et al., 2006).

Forensic accounting represents an integration of accounting, auditing and investigative skills that

support the acquisition, maintenance, and analysis of relevant information in a manner that would be

acceptable for judicial review and meet the requirements of professional oversight. It also extends to

the formulation and presentation of findings in formal reports and court testimony as an expert

witness. Forensic accountants command a set of skills that transcends the traditional expectations of

accountants. These skills are acquired and enhanced through audit experience and increased

investigative training. This allows the forensic accountant to analyze and interpret more complex

business and non-business issues in a manner that meets the highest requirements of reliability and

integrity. As such, forensic accountants may be employed in a public or private capacity and play

important roles in internal auditing departments of banks and insurance companies, governmental and

law enforcement agencies, and as self-employed contractors for individuals and attorneys. Thus, the

market for forensic accountants and the required skill sets are very well defined.

4. COMPUTER FORENSICS COURSE EXERCISES AND PROJECTS

Forensic accountants are often deficient in the understanding of computer forensics for several

reasons. Many schools do not offer such a course because they lack qualified instructors. Also, the

topics are not covered on the CPA exam and a large percentage of accounting students plan to acquire

a CPA or similar certification such as CMA or CIA, none of which require the technical skills of

computer forensics. Finally, accounting students who plan to take the CPA exam may have to meet the

150 hour rule adopted by many states and may see forensic skills as ones they can acquire in the future

(Seda et al., 2008).

This deficiency, however, directly impacts the ability and effectiveness of the forensic accountant and

makes him or her more reliant upon IT for all steps requiring computer forensic analysis. Also,

students may recognize that the computer forensic skills are special and may lead to careers in forensic

accounting and IT auditing. Educators who recognize the importance of computer forensic skills will

be interested in exercises and projects that provide the accounting student with basic computer

forensic techniques. The exercises and projects that follow introduce several widely recognized

software products that are important to forensic analysis. Among other things, these projects illustrate

how fraudsters can hide important information in files, how to inspect files for hidden data, how to

acquire images from a suspect drive, how to recover deleted files and how to calculate hash values to

ADFSL Conference on Digital Forensics, Security and Law, 2014

146

insure the integrity of files. A set of student files for the exercises and projects are available upon

request from the author.

4.1 Exercise and Project Requirements

The projects use several applications available in demo versions.

1. WinHex Hexadecimal Editor: http://download.cnet.com/WinHex/3000-2352_4-10057691.html

2. AccessData FTK Analyzer: http://www.accessdata.com/support/product-downloads/ftk-download-

page

3. HashCalc: http://download.cnet.com/HashCalc/3000-2250_4-10130770.html

4. Eraser: http://download.cnet.com/Eraser/3000-2092_4-10231814.html

The following files are used in the exercises and projects and can be downloaded in zipped format.

They should be placed in a work-folder named Projects.

4.2 Computer Forensic Exercises

These exercises are intended to introduce the accounting student to knowledge and skills basic to

computer forensics. All of the exercises are short and can be performed in-class or as take-home

assignments.

Exercise 1: Numbering Systems

Tantamount to the use of forensic software is the knowledge of the binary and hexadecimal numbering

systems. All modern numbering systems have two things in common: (1) digits, and (2) placeholders.

Each placeholder represents the base raised to a higher power. In the following tables, the second row

is the placeholder and the third row is the power to which each value is raised. In the first

Placeholder and Power

(Note that the power is always one less than the placeholder.)

10

9

8

7

6

5

4

3

2

1

9

8

7

6

5

4

3

2

1

0

DECIMAL (Base 10 - Ten digits 0-9)

ADFSL Conference on Digital Forensics, Security and Law, 2014

147

Placeholder and Power

10

9

8

7

6

5

4

3

2

1

10

9

10

8

10

7

10

6

10

5

10

4

10

3

10

2

10

1

10

0

Thus, in base 10, the value 8,673 equals:

8 x 10

3

+ 6 x 10

2

+ 7 x 10

1

+ 3 x 10

0

= 8,000 + 600 + 70 + 3

BINARY (Base 2 – Two digits 0 and 1)

Placeholder and Power

10

9

8

7

6

5

4

3

2

1

2

9

2

8

2

7

2

6

2

5

2

4

2

3

2

2

2

1

2

0

Thus, in base 2, the value 1100 1100 equals:

1 x 2

7

+ 1 x 2

6

+ 1 x 2

3

+ 1 x 2

2

= 128 + 64 + 8 + 4 = 204

base10

HEXADECIMAL (Base 16 - Sixteen digits 0-F where A=10, B=11, C=12, D=13, E=14, F=15)

Placeholder and Power

10

9

8

7

6

5

4

3

2

1

16

9

16

8

16

7

16

6

16

5

16

4

16

3

16

2

16

1

16

0

Thus, in base 16, the value 1A5F equals:

1 x 16

3

+ 10 x 16

2

+ 5x 16

1

+ 15 x 16

0

= 4096 + 2560 + 80 + 15 = 6,751

base10

Student Exercises:

Answers (in decimal values)

Convert each of the following to decimal values.

1. Binary: 1111

2. Binary: 1111 1111

3. Binary: 1 0000 0000

4. Binary: 1010 1010

5. Hex: 123

6. Hex: ABC

7. Hex: FF

8. Hex: 100

1. 15

2. 255

3. 256

4. 170

5. 368

6. 2748

7. 255

8. 256

Exercise 2: Creating Hash Values (Checksums)

A hash, also known as a checksum, is a value that has no real meaning. Hashes are often used as

control values such as the sum of employee id numbers for payroll applications. In accounting and

forensics, hash values are created by computer algorithms that create a unique key string for any size

of file. In most of our projects we would hash the file before and after testing to insure that the file

itself has not been modified in any way.

The file size has no impact on the string length which is determined by the algorithm. In forensics the

algorithms, MD5 and SHA1 have been popular. Calculators are readily available. We use HashCalc.

ADFSL Conference on Digital Forensics, Security and Law, 2014

148

1. Open HashCalc© and note the number of hash types. Open the MS Word file ID Theft.

2. Select the MD5, SHA1 and Tiger hash algorithms. Click Enter.

3. Take a screenshot of the results and add to your Results file and save to your Project_Work

folder. See Figure 1.

4. Close the ID Theft file.

5. Open the ID Theft file and again select the MD5, SHA1 and Tiger hash algorithms. Click

Enter.

6. Compare the results to those from your previous screenshot. They should be the same.

7. At the bottom of the file type OK. Save the file.

8. Open the ID Theft file and again select the MD5, SHA1 and Tiger hash algorithms. Click

Enter.

9. Compare the results to those from your previous screenshot. They should be the different.

Figure 1 Original Hash Values for ID_Theft.doc

Exercise 3: Using Command Prompt

IP and MAC Addresses for Windows OS

IP (Internet protocol) addresses are not unique to computers. They identify the node. If you switch

computers the IP address remains with the node. However, each computer has a unique identifying

number called the MAC (media access control) address. In this exercise you will use the Command

Prompt to find your IP and MAC addresses.

On your home computer, go to Accessories / Command Prompt

If the cursor is not on the C: directory, enter the following…

ADFSL Conference on Digital Forensics, Security and Law, 2014

149

CD\

Then enter …

Ipconfig /all

Find the physical address (MAC address) and the IPv4 address and write them down.

Command Prompt and DOS Commands

At the command prompt attempt the following commands. [ ] is for annotation only.

This assumes the file is on your C: drive. If not, then insert the full path to the file.

Enter the following commands

C: [this will take you to the c: drive]

TYPE C:\ Shakespeare.txt [this will type out the contents of the file]

RENAME C:\ Shakespeare.txt WilliamShakespeare.txt [renames the file]

MD Projects [creates a new folder name Projects]

RD Projects [removes folder named Projects]

DIR *.* [lists all files in the current folder]

DIR C:\Projects\ *.doc [lists all .doc files in the Projects folder]

PrintScreen the CommandPrompt window.

Enter the following command to clear the screen: CLS

Access and Print System Information

Click Start \ Run and type msconfig

In the System Configuration table select Startup and examine what programs are opened when you

start your computer. Do you want all of these to open? If not, then deselect the box for unwanted

applications.

In the System Configuration table select Tools\Security Center and click Launch. Click Internet

Options and explore the trusted certifications.

PrintScreen the System Information for your computer.

Exercise 4: File Signatures

Opening files in either NotePad or a hexadecimal (hex) editor provides initial information for

examination of files. The investigator can also determine if the file type is correct. For each file, you

will open it in both NotePad and WinHex. In WinHex you will note the first eight bytes in positions 0-

7. Each byte will be two characters ranging from 00-FF. These eight bytes often are the signature for

the filetype. However, for MS Windows, the signature is the same for Word, Excel and PowerPoint

but different for Access. To determine the filetype you must do a find (Ctrl+F) and search for Word,

Excel or PowerPoint. Figure 2 shows the first eight bytes for a Word file and the result of a Find

operation.

Step 1: Create a work-folder on your personal computer c: drive named Projects.

Step 2: Download and extract the projects.zip from the instructor’s web site.

Step 3: Open the following files in both Notepad and WinHex. Determine the file type for each and

indicate how you could identify the file type in Notepad and the hex editor. Simply copy the

identifying information into the table. If it does not appear to be identifiable then type NI.

The hex signatures have been completed in the table below.

ADFSL Conference on Digital Forensics, Security and Law, 2014

150

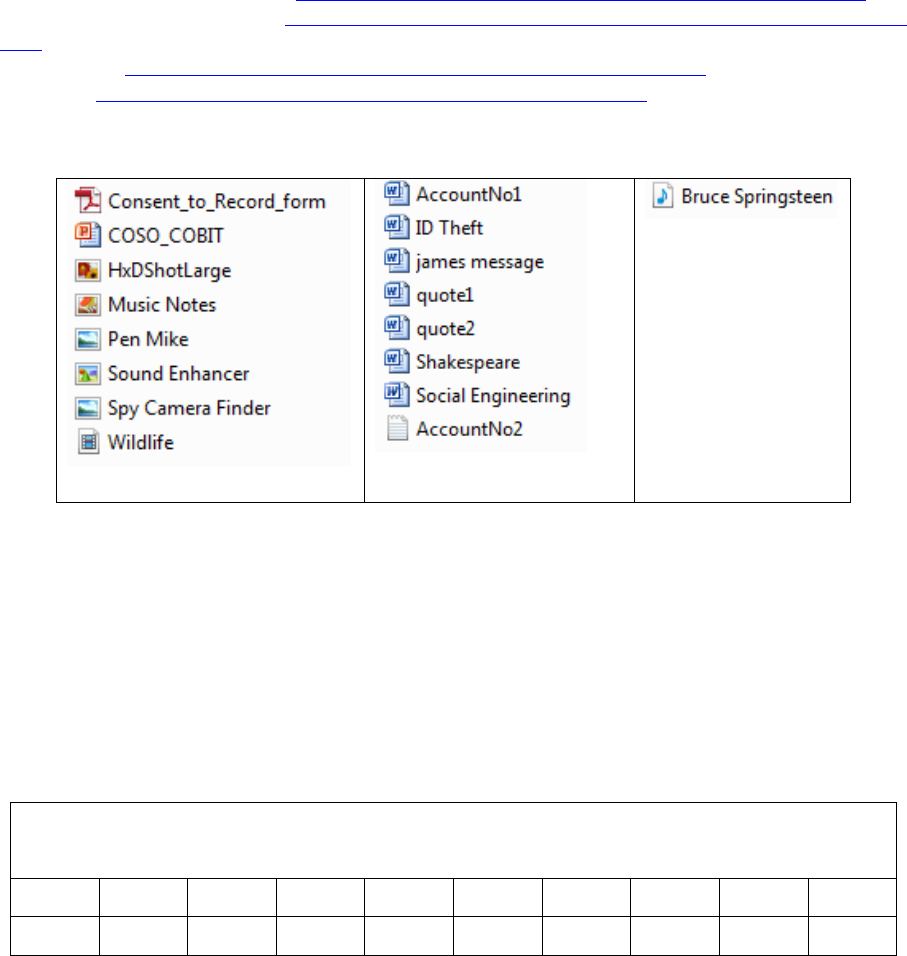

File

Filetype

NotePad

Hex Editor

Consent_to_Record_Form

.pdf

25 50 44 46 2d 31 2e 34

HxDShotLarge

.png

89 50 4E 47 0D 0A 1A 0A

Sound Enhancer

.gif

47 49 46 38 39 61 90 01

Social Engineering

.doc

DO CF 11 E0 A1 B1 1A E1

Pen Mike

.jpg

FF D8 FF E1 2F FE 45 78

AccountNo2

.txt

54 68 65 20 62 61 6E 6B

Bruce Springsteen

.mp3

49 44 33 03 00 00 00 03

Wildlife

.wmv

B7 D8 00 20 37 49 DA 11

Step 4: Open the Social Engineering file in WinHex and change the first eight bytes to resemble a .jpg

file. Save the file and then try to open it. What happens? Open it again in WinHex and change the first

eight bytes back to their correct values. Save and re-open. It is now back to its original state. This

process allows fraudsters to conceal files in plain sight.

The following signature is the same for MS Windows Excel, Word, and PowerPoint

The following shows the result of a Find operation for Word in the file. Use the ASCII table to show how

Microsoft Word is represented in hex.

Figure 2 File Signature for MS Word, Excel and PowerPoint

Exercise 5: ASCII Codes

ASCII code is used for storage of all text values in personal computers. In ASCII each letter, digit and

special character is represented in eight bits or one byte. From the table in Figure 3, verify that you

understand the ASCII code by determining the code for each item in the table below. Leave a space

between each byte. Note in the first example, the space requires a code.

ITEM

ASCII VALUE IN HEX

MI 5

4D 49 20 35

Microsoft Word

123 Oak Ave.

(555) 123-1234

$50.46

ADFSL Conference on Digital Forensics, Security and Law, 2014

151

Figure 3 ASCII Code (Source: http://ascii.cl/)

4.3 Computer Forensic Projects

Forensic Project 1: Working with Image Files

A basic tenant of forensic investigations is never work on the original file. First create a mirror image

(bit-by-bit copy) and work on the copy. In this exercise the student will image the contents of a USB

drive (the suspect drive) and perform a search on the image file.

Learning Goal(s): Wiping Disks, Creating a USB Image File; Searching an Image File

Software: Eraser, ProDiscover Basic

Files: Shakespeare, james message, ID Theft, quote1, quote2, AccountNo1, AccountNo2,

COSO_COBIT, Social Engineering, Sound Enhancer, Pen Mike, Spy Camera Finder, Consent to

Record Form

First, you will delete the files on your USB drive and then add the files you wish to have in your image

file. Be sure that you have saved your USB files to another drive.

ADFSL Conference on Digital Forensics, Security and Law, 2014

152

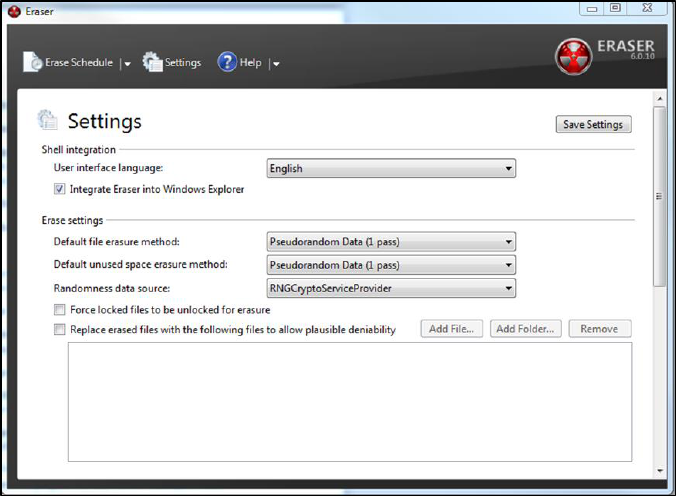

1. Start Eraser and be sure that the correct drive is selected. In settings, choose those for

Pseudorandom 1 Pass (see Figure 4). Run Eraser.

2. Copy the above files to your USB drive.

3. Start ProDiscover Basic and click Run Administrator. In the Launch Dialog box, click the

New Project tab and enter the project number Proj01, and project name Proj01.

4. Click Action and click Capture Image. For Source Drive, select your USB drive. For

Destination also select your USB drive. Name the destination file ForensicProject. Use your

initials for Technician Name and 01 for image number. Click OK. This may take several

minutes. An image file (ForensicProject.eve) will be created which will be a bit-by-bit copy

of your USB.

5. Start ProDiscover Basic and click Run Administrator. In the Launch Dialog box, click the

New Project tab and enter the project number: Proj01, and project name:

6. Click Action from the menu, point to Add and click Image File.

7. In your work folder, click the file ForensicProject.eve and then click Open. If the Auto Image

Checksum message box opens, click No (we will not calculate a checksum on this project).

8. In the tree view, click to expand Content View, click to expand Images, and then click the

pathname containing your image file. (Files are listed in the work area. See Figure 5).

9. Right-click any file and click View – this will start the associated program such as MS Word

or Excel. View the file and then exit the program. Try this with several types of files.

10. To search for the keyword “bank” click the Search toolbar button (the binoculars icon) to open

the Search dialog box.

11. Click the Content Search tab. If necessary, click the ASCII button and the Search for the

Pattern(s) option button. Type bank in the list box for search keywords. Under Select the

Disk/Image(s) click the drive that you are searching and then click OK.

12. In the tree view, click to expand Search Results and then click Content Search results to

specify the search type and note the search results in Figure 6.

13. To search all clusters, click the Cluster Search tab and search for bank. This will take more

time because all clusters are being searched. Note the results.

14. Save the project. Click File, Save Project from the menu.

Figure 4 Eraser Settings

ADFSL Conference on Digital Forensics, Security and Law, 2014

153

Figure 5 Expanded Path in Content View

Figure 6 Search for the Term “Bank”

Forensic Project 2

Learning Goals: Search a Unix .dd image file for hidden account numbers

Software: ProDiscover Basic

Files: RawFormat.dd

1. Start ProDiscover Basic and click Run Administrator. In the Launch Dialog box, click the

New Project tab and enter the project number Proj02, and project name Proj02. Click File,

Save Project.

2. Click Action from the menu, point to Add and click Image File.

3. In your work folder, click the file RawFormat.dd and then click Open. If the Auto Image

Checksum message box opens, click No (we will not calculate a checksum on this project).

Note that this is a Unix .dd image file.

ADFSL Conference on Digital Forensics, Security and Law, 2014

154

4. In the tree view, click to expand Content View, click to expand Images, and then click the

pathname containing your image file. (Files are listed in the work area.)

5. Click View, Gallery View. Scroll through the graphics files on the drive image. To discover

the account numbers you will have to inspect each of these files. In the Add Comment dialog

box enter a brief comment and click OK. This will add your case notes to the ProDiscover

reports.

6. For each file of interest, open the file click the Search toolbar button (the binoculars icon) to

open the Search dialog box.

7. Click the Content Search tab. If necessary, click the ASCII button and the Search for the

Pattern(s) option button. Type the account number 0102030405 in the list box for search

keywords. Under Select the Disk/Image(s) click the drive that you are searching (see Figure7)

and then click OK.

8. In the tree view, click to expand Search Results and then click Content Search results to

specify the search type and note the search results.

9. To search all clusters, click the Cluster Search tab and repeat the search using the account

number 0102030405 as the search keyword. Enter notes in the Add Comment dialog box

when your search is successful.

10. Click Report in the tree view and review the report to insure it is complete. A complete and

concise report is critical to the forensic investigation.

11. Click the Export toolbar button. In the dialog box click the RTF Format button (for rich

text) and type Bank Account Report in the File Name text box, and then click OK. You have

now saved the project report.

Figure 7 Image File Displayed in Work Area

Forensic Project 3

Learning Goals: Extract allocated files and unallocated files separately

Software: ProDiscover Basic

Files: ForensicProject.eve

1. Start ProDiscover Basic and click Run Administrator. In the Launch Dialog box, click the

New Project tab and enter the project number Proj03 and project name Proj03. Then click

Open.

ADFSL Conference on Digital Forensics, Security and Law, 2014

155

2. In the tree view, click to expand Add, click Image File. In your work folder, click the

ForensicProject.eve file and then click Open and click No in the Auto Image Checksum

message box. Save the project to your folder.

3. In the tree view, click to expand Content View, click to expand Images, and then click the

pathname containing the image file. Examine the files displayed in the work area. Under the

column heading Deleted note that the files are either YES (indicating deleted or unallocated

files) or NO (indicating active or allocated files).

4. Sort on the Deleted column by clicking the Deleted header.

5. To extract the allocated files, right-click each of the files designated as NO in the Deleted

Column and click Copy File. In ProDiscover Basic this must be performed for each separate

file.

6. To extract the unallocated files, right-click each of the files designated as YES in the Deleted

Column and click Copy File. As you click a check-box, the Add Comment dialog box

appears. Note the filename and type that has been deleted. (In practice, you would first

examine each of these files and add a meaningful comment.)

Forensic Project 4

This project creates two desk-top icons that enable or disable writing to USB devices. Students are

advised to create a system restore point before attempting this project.

Learning Goals: Modify the MS Windows Registry; Create a USB Write-Blocker

1. Software: MS Windows Regedit

1. In the MS Windows Start Search text box, type regedit and press Enter. This opens the

Registry Editor from which you can access system folders and files.

2. In the editor, browse to and click to expand the

\HKEY_LOCAL_MACHINE\SYSTEM\CurrentControlSet key.

3. Right-click the Control subkey, click New.

4. The Registry Editor prompts the user for a key name. Enter USBDevicePolicy and press

Enter. This creates a descendant key.

5. Right-click the USBDevicePolicy key, point to New, and click DWORD Value. If you have

an option for 32-bit or 64-bit, click 32-bit.

6. In the prompt, type WriteProtect and press Enter.

7. In the key data area, right-click WriteProtect DWORD (or just WriteProtect) and click

Modify.

8. In the Edit DWORD Value dialog box, change the Value Data setting from 0 to 1, and then

click OK to activate write-blocking to USB devices.

9. Right-click the USBDevicePolicy descendant key and click Export.

10. In the Export Registry File dialog box, click Desktop in the Save in list box. In the filename

text box, type Write Protect USB ON, and click Save.

11. In the registry editor, click USBDevicePolicy. In the key data area, right-click WriteProtect

DWORD and click Modify.

12. In the Edit DWORD Value dialog box, change the Value Data setting from 1 to 0 and click

OK to deactivate write-blocking to USB devices.

13. Right-click USBDevicePolicy descendant key again and click Export.

14. In the Export Registry File dialog box, click Desktop in the Save in list box. In the File name

text box, type Write Protect USB OFF, and click Save. Close the registry editor.

Forensic Project 5

Learning Goals: Restore an image file to a drive using the UNIX dd format for raw acquisition.

Software: ProDiscover Basic

ADFSL Conference on Digital Forensics, Security and Law, 2014

156

Files: ForensicProject.eve

1. Transfer the data from the ForensicProject.eve file to the target drive (USB drive). Connect a

USB drive to the workstation. Smaller USB drives work best as this exercise writes to the

entire drive. I suggest 100-500 MB if available.

2. Start ProDiscover Basic and click Tools, Copy Disk.

3. In the dialog box click the Image to Disk tab.

4. From the work folder, click the ForensicProject.eve file and then click Open.

5. In the Copy source disk dialog box click in the area below Disk Name.

6. Click the Disk Name list arrow and then click the target drive, then click OK.

7. In the dialog box that opens click Write all 0’s and then click OK. This begins the data

loading and fills the remainder of the drive with 0’s.

8. In the completion dialog box click OK to terminate loading.

1. Now you will use the raw acquisition format for creating an image file.

9. On your workstation click the Write Protect USB ON icon that you created earlier. This will

protect the acquisition drive. Click Yes and then OK in the confirmation dialog boxes.

10. In ProDiscover Basic click Action, Capture Image from the menu.

11. In the dialog box, click the Source Drive list arrow and then click PhysicalDrive1.

12. Next to the Destination text box, click the >> button and in the Save As dialog box navigate to

the work folder and click Save.

13. In the Capture Image dialog box click the Image Format list arrow and click UNIX style dd

format (for a raw acquisition). Click OK to start the acquisition and then click Proceed in the

warning box. When the acquisition is complete click OK in the message box. The raw format

creates the acquired file (.dd), a log file (.pds) and a hash file (.md5).

14. Click the Write Protect USB OFF button on the workstation desktop and remove the USB.

Exit ProDiscover Basic. The suspect files are now imaged on the workstation in UNIX dd

format.

Forensic Project 6

Learning Goals: How to locate time and date information from metadata; How to identify file

fragments found in the MFT records which could be found in unallocated disk space or the

Pagefile.sys.

Software: ProDiscover Basic

1. Open Notepad and create a text file with the message: Not even computers will replace

committees because committees buy computers. Save the file in the work folder as

ForensicProj06A.txt. Exit Notepad.

2. Start ProDiscover Basic and begin a new project ForProj01A. Click Action and then Add.

3. In the Add Disk to Project dialog box click PhysicalDrive0. Type c-drive in the text box and

click Add. If there is a warning message, click OK.

4. In the tree view, click to expand Content View, Disks, and PhysicalDrive0. Then click the C

drive.

5. If necessary scroll down in the work area and right-click $MFT and click Copy File. In the

Save As dialog box, save the file to the work folder. Exit ProDiscover Basic.

6. Start the WinHex hex editor by clicking Start, All Programs, WinHex. If there is a warning

message box, click OK.

7. On the toolbar click Open and navigate to the workfolder. Click the $MFT file and then

Open.

8. On the menu, click Search, Find Text.

9. In the text box for specifying a search string type ForensicProj06A.txt. Click the Format

Code arrow, click Unicode and then click OK.

ADFSL Conference on Digital Forensics, Security and Law, 2014

157

10. Right-click the Data Interpreter window and click Options. In the dialog box, click the

Win32 FILETIME (64 bit) check box and then click OK.

11. Scroll up so that the MFT record label FILE for ForensicProj06A.txt is the first line at the

top of the hexadecimal and text displays.

12. Click at the beginning of the record, on the letter F in FILE, and then drag down and to the

right while you watch the hex counter in the lower-right corner. When the counter reaches 50

release the mouse button.

13. Move the cursor to the next byte (one position to the left) and record the date and time of the

Data Interpreter’s FILETIME values.

14. Exit WinHex.

Forensic Project 7

Learning Goals: Conducting a keyword search

Software: AccessData FTK

1. Start AccessData FTK. Create a new case called ForProj08 for the case name and number.

Click Next until the Add Evidence and Case dialog box appear.

2. Click Add Evidence, click Local Drive and then click Continue.

3. Insure that your USB drive (or local disk drive) and Logical Analysis are selected and then

click OK.

4. In the Evidence Information dialog box click to select your time zone and then click OK.

Click Next and then click Finish. FTK will process the files and then indicate the evidence

items.

5. Click Search, Tools, Analysis Tools from the menu, click to select the Full Text Indexing

check box and then click OK.

6. In the search term text box type Diamond and then click Add. Click the View Cumulative

Results button and then click OK in the Filter Search Hits dialog box. Repeat the search for

the terms Gold, and Silver. The number of hits or occurrences of the search terms will appear

under Search Items. (This will not include the items in the file slack space.)

7. Click Overview, Documents and then click. Scroll the upper-right pane until you see the

word ‘Diamond’. Note the logical sector position at the bottom of the upper-right pane.

8. Click the Search tab and then click Live Search. In the text box, type Diamond and make

sure that ASCII and UNICODE are selected. Click Add and then the Search button, select

All Files option and then click OK. When the search is complete click View Results to see

the information displayed at the upper-right.

9. Click the expand (+) buttons to find the search results. Scroll in the middle pane until you find

‘Diamonds’.

10. Repeat steps 8 and 9 for ‘Gold.’

11. The bottom pane displays details about the data FTK found including each occurrence of the

word. Close FTK.

Forensic Project 8

One way of hiding information is to place the information in a file using a hex editor and corrupt the

file so that it cannot be opened or, when opened, presents garbled data. This can be performed by

simply rotating the bits in the file. To repair the file, simply rotate the bits back to their previous

position.

Learning Goals: Bit shifting and rotation.

Software: AccessData FTK

Files: AccountNo2.txt

ADFSL Conference on Digital Forensics, Security and Law, 2014

158

1. Start WinHex and open the file codes.txt.

2. Move the cursor over the toolbar buttons for Shift Left, Shift Right and note that Rotate Left,

Rotate Right, Block Shift Left and Block Shift Right are also available. Click Rotate Right

and create a screen print of the results for later comparison. Assume that the data is ordered in

little endian. Then click OK.

3. Click Rotate Left. In the Rotate Left Operation dialog box insure that the settings are the

same as in the Treat Data As for Rotate Right. Otherwise, the bits will not be shifted

equally. Save the file but do not close.

4. Click Shift Right and click OK twice and note what is happening with the data.

5. Click Block Shift Left. Attempt to reverse the procedure by clicking Block Shift Right, click

Shift Left twice and click OK as needed.

6. Note that the data is garbled and the procedure has not been reversed. A shift (nonrotated)

operation simply drops the bits as they are moved to the right or left and they cannot be

recovered. Close the file but do not save. See Figures 8 and 9.

Figure 8 File Before Bit Shifting

Figure 9 File After Bit Shifting

ADFSL Conference on Digital Forensics, Security and Law, 2014

159

5. DISCUSSION AND CONCLUSIONS

This paper addresses the need for computer forensics education for accounting students. While the

forensic accounting profession continues to grow, most accounting students do not have exposure to a

class in computer forensics. To be effective, it is essential that forensic accountants be knowledgeable

of and able to apply basic computer forensic skills. The purpose of this paper is to present the educator

with a number of exercises and projects that provide the accounting student with skills important to

careers as forensic accountants and IT auditors. While students may not emerge from this course as

experts in computer forensics they would develop and important competence that would benefit the

organization. These skills could be extended in a variety of ways through pursuing advanced education

in college courses, workshops and self-study tutorials.

REFERENCES

AICPA. (2013). Retrieved on July 20, 2013 from

http://www.accountingtoday.com/gallery/AICPA2012-Top-10-Technology-Initiatives-62024-1.html).

AICPA. (2013). Statement on Audit Standards 99, consideration of fraud in a financial statement

Audit. Retrieved January 15, 2014 from

http://www.aicpa.org/Research/Standards/AuditAttest/DownloadableDocuments/AU-00316.pdf

Casey, E. (2011). Digital evidence and computer crime: Forensic science, computers, and the

Internet, 3

rd

ed. Elsevier Science & Technology.

Coglitore, F.J. & Matson, D.M. (2007). The use of computer-assisted auditing techniques in the

auditing course: Further evidence. Journal of Forensic Accounting, VIIII, 201-226.

Davis, C., Schiller, M. & Wheeler, K. (2007). IT Auditing, New York, NY: McGraw-Hill.

Hall, J., & Singleton, T. (2005). Information Technology and Assurance, 2

nd

ed. Thomson South-

Western, Mason, OH.

Hurt, B. (2007). Teaching what matters: A new conception of accounting education. Journal of

Education for Business, 82(5), 295-299.

Kearns, G. (2010). Computer forensics for graduate accountants: A motivational curriculum approach.

Journal of Digital Forensics, Security and Law, 5(2), 63-83.

LA Times. Target Traces Data Breach to Credentials Stolen from Vendor. Retrieved January 28, 2014

from:http://www.latimes.com/business/money/la-fi-mo-target-data-breach-vendor-

20140129,0,8026.story#axzz2rzEFEbhQ

Merhout, J. W. & Buchman, S. E. (2007). Requisite skills and knowledge for entry-level IT auditors,

Journal of Information Systems Education, 18(4), 469-477.

Nelson, B., Phillips, A., & Steuart. C. (2010). Guide to Computer Forensics and Investigations, 4

th

ed.

Boston, MA: Cengage.

O'Donnell, J. & Moore, J. (2005). Are accounting programs providing fundamental IT control

knowledge? The CPA Journal, 75(5), 64-66.

PCAOB (Public Company Accounting Oversight Board) (2005). Staff questions and answers on

auditing standard No. 2: Internal Control. Retrieved on Nov 15 2013 from

http://pcaobus.org/Standards/QandA/06-23-2004.pdf

Pearson, T. A. & Singleton, T. W. (2008). Fraud and forensic accounting in the digital environment,

Issues in Accounting Education, 23(4), 545-559.

ADFSL Conference on Digital Forensics, Security and Law, 2014

160

Sammons, J. (2012). The basics of digital forensics: The primer for getting started in digital forensics.

Elsevier Science & Technology.

Seda, M., Kramer, B., & Peterson, K. (2008). The emergence of forensic accounting programs in

higher education. Management Accounting Quarterly, 9(3), 15-23.